Introduction

Non-qualified mortgage (Non-QM) loans are no longer a niche product. In 2025, they’ve become an essential offering for mortgage professionals looking to serve a diverse range of borrowers—including the self-employed, real estate investors, retirees, and foreign nationals. As economic realities shift and traditional borrower profiles evolve, Non-QM has grown into a multi-billion-dollar sector of the mortgage industry. Yet despite its maturity, many brokers, borrowers, and referral partners still hesitate to engage with Non-QM lending due to lingering myths and outdated assumptions.

This article sets the record straight. We’ll break down the five most common myths about Non-QM loans, back each one with real-world data and industry insight, and explain why mortgage professionals should embrace Non-QM lending with confidence and strategic foresight.

To further support brokers and loan officers navigating this rapidly expanding space, we’ll also provide key data, borrower use cases, and practical strategies to help demystify Non-QM lending and unlock new business opportunities.

If you’re a broker, correspondent, or loan officer looking to grow your pipeline, expand your referral network, and win deals that traditional lenders can’t, this guide is for you.

Myth #1: “Non-QM Loans Are Risky Like Subprime Mortgages”

This is perhaps the most damaging and persistent myth surrounding Non-QM. The association with the 2008 housing crash continues to influence perceptions—but it’s time to update the narrative.

Reality: Non-QM loans are not subprime. In fact, they are fully underwritten, carefully priced, and designed for borrowers who fall outside the rigid constraints of Qualified Mortgage (QM) guidelines. Subprime lending prior to the Great Recession was marked by no-doc loans, predatory teaser rates, and systemic disregard for a borrower’s ability to repay. In contrast, today’s Non-QM products:

- Comply with the Ability to Repay (ATR) rule under Dodd-Frank

- Require thorough documentation (e.g., bank statements, CPA-prepared P&Ls, asset statements)

- Are underwritten using common-sense criteria, not automated overlays

- Are often issued to borrowers with FICO scores in the 700+ range

According to CoreLogic and S&P Global, Non-QM loans originated after 2015 have demonstrated exceptional performance, with delinquency rates well below government-backed loans. In many cases, default rates are under 1.5%, compared to 3–5% for FHA and VA loans during the same periods.

Modern Non-QM lending is risk-managed, transparent, and attractive to both borrowers and investors. The comparison to subprime is simply false.

Myth #2: “Non-QM Loans Are Only for Low-Credit or Desperate Borrowers”

Reality: Many Non-QM borrowers are actually well-qualified, financially stable individuals who need flexibility—not forgiveness.

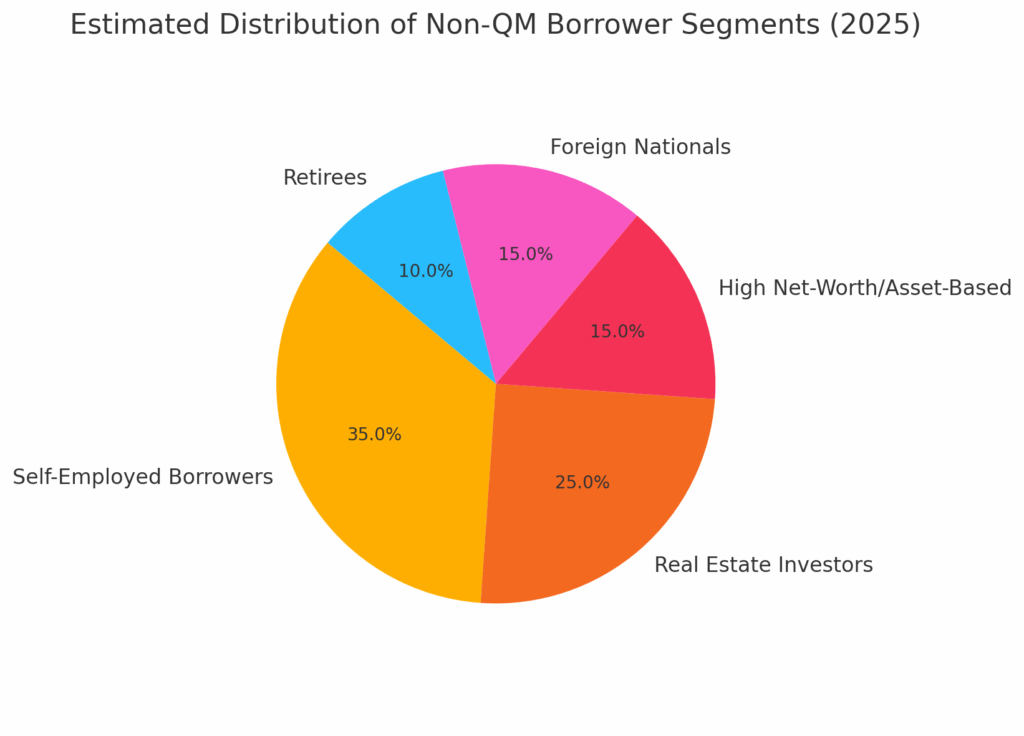

The borrower profiles that benefit from Non-QM include:

The borrower profiles that benefit from Non-QM include:

- A self-employed business owner with $500K+ in annual income, but limited taxable income due to deductions

- A real estate investor with a strong portfolio and 800 FICO, seeking a DSCR loan

- A physician launching a private practice with limited W-2 history but strong liquidity

- A retiree with significant assets and no traditional income stream

- A foreign national purchasing a U.S. investment property with 50% down

Non-QM loans cater to structurally complex borrowers, not substandard ones. These clients often:

- Put more money down (20–40% LTV)

- Have high reserves and assets under management

- Prioritize privacy, flexibility, and speed

In AHL’s TPO pipeline, a majority of Non-QM borrowers have FICO scores above 700. And more than 65% of these loans exceed $500,000 in loan size, with many approaching or surpassing jumbo loan thresholds.

This is a high-value client base—one that brokers should actively pursue.

Myth #3: “Non-QM Loans Are Difficult to Close”

Reality: While Non-QM loans require a different approach, they are not inherently harder to close. The key difference lies in the structure and documentation, not in the volume of work.

In fact, with the right tools and support, many brokers find Non-QM loans easier to manage than ultra-strict agency loans.

For example:

- Bank statement loans require 12–24 months of statements and a calculation of average monthly deposits, not tax returns

- DSCR loans use property rents and expenses to qualify—not borrower income

- Asset depletion loans involve verifying account balances and seasoning, then applying an income calculation factor

These processes are repeatable once understood. At AHL, expert AEs, automated calculators, and pre-approval pipelines streamline Non-QM deals from application to closing.

Average Non-QM closings range from 21 to 30 days, with some loans funding in under three weeks when prepared by experienced teams. Broker tips for faster closings:

- Use lender-provided tools to pre-calculate income

- Package documents in advance—including letters from CPAs, leases, and reserves

- Avoid mid-loan changes in property type, occupancy, or structure

With the right lender partner, Non-QM becomes a fast, profitable, and highly repeatable source of business.

Myth #4: “There’s No Market or Demand for Non-QM Loans”

Reality: Non-QM lending is not just in demand—it’s one of the fastest-growing segments of the mortgage industry.

According to S&P Global and Nomura, Non-QM loan originations in the U.S. reached $45 billion in 2023, up from $34 billion in 2022. Projections suggest this will exceed $75 billion annually by 2026, driven by:

- The rise of the gig economy (freelancers, consultants, digital entrepreneurs)

- Expansion in the real estate investor segment, especially short-term rentals and Airbnbs

- Retirees and high-net-worth individuals seeking to leverage assets without income

- Foreign national investment in U.S. real estate as a safe haven asset class

Broker channels are playing a central role in this shift. In markets like California, Texas, Arizona, and Florida, Non-QM makes up over 15% of new purchase originations, according to ICE Mortgage Technology.

And this demand isn’t slowing. As underwriting becomes more data-driven and more borrowers seek speed and customization, Non-QM will continue to capture market share from conventional agency loans.

Myth #5: “Secondary Markets Don’t Want Non-QM Loans”

Reality: Secondary markets actively pursue Non-QM paper—especially high-quality, well-structured loans.

Private-label mortgage-backed securities (MBS) backed by Non-QM loans have gained momentum in recent years with several firms securitizing billions in Non-QM paper with strong investor demand. These MBS are attractive for several reasons:

- Strong yields compared to agency paper

- Built-in credit enhancements and low average LTVs

- Loans backed by real estate and full documentation of ability to repay

In 2024, Non-QM MBS issuance reached an all-time high, with over $35 billion securitized in the private-label market. These transactions were oversubscribed, and rated tranches received stable outlooks from Fitch and Moody’s.

Why does this matter for brokers?

- It ensures capital availability and stable pricing

- It validates the long-term sustainability of Non-QM as a product category

- It increases lender capacity to fund and close loans faster

In short, the capital markets are not just accepting Non-QM—they’re banking on it.

Borrower Spotlights—Who Benefits from Non-QM Lending?

To better understand the real-world utility of Non-QM lending, let’s look at a few borrower scenarios that highlight how flexible products change outcomes.

- The Self-Employed Creative

- Profile: A freelance UX designer earning $200K annually from multiple clients

- Challenge: Low adjusted gross income due to aggressive deductions

- Solution: A 12-month personal bank statement loan

- Outcome: Approved for a $750,000 home with 15% down and no MI

- The Real Estate Investor

- Profile: Owns six rental properties and is acquiring a new duplex

- Challenge: Needs loan qualification based on cash flow, not income

- Solution: DSCR loan with 1.20x coverage ratio, no W-2 or tax returns

- Outcome: Closed in 21 days using rental income from subject property

- The Retiree Relocator

- Profile: Retired corporate executive relocating to be near grandchildren

- Challenge: No employment income, high liquid reserves

- Solution: Asset depletion loan based on $1.5M in brokerage accounts

- Outcome: Approved for $950,000 home in Florida with no DTI consideration

- The Foreign National Investor

- Profile: Canadian entrepreneur investing in Florida rental market

- Challenge: No U.S. tax ID or credit history

- Solution: Foreign national loan with 35% down, no income documentation

- Outcome: Secured property with cash flow analysis and local management agreement

These examples showcase how Non-QM lending bridges the gap between financial reality and homeownership/investment goals for a wide array of qualified borrowers.

Practical Tips: How to Talk to Borrowers About Non-QM

Many consumers have never heard of Non-QM—or they assume it means subprime or high risk. Educating them with clarity is key. Here are talking points brokers can use to simplify the conversation:

- “This loan is for strong borrowers with non-traditional income—like business owners or retirees.”

- “We don’t need tax returns. We’ll use your bank deposits to show income.”

- “This is a real loan. You own the home, and it works like any other mortgage.”

- “These loans close fast and are underwritten manually by people, not computers.”

- “You may pay slightly more in rate, but you avoid the headaches and limitations of agency loans.”

Keep the focus on the outcome: qualifying for the right home, with the least friction, in a structure that works for the borrower’s real financial life.

Non-QM and the Future of Lending

As the traditional 30-year fixed agency loan continues to face pressure from changing demographics, housing demand, and labor shifts, Non-QM will become even more central to the mortgage industry. The loan officer of the future is not just a conforming guideline expert—they’re a lending strategist who knows how to structure, package, and guide borrowers through customized options.

Non-QM is not a detour—it’s a direction. And mortgage professionals who embrace it now will lead the conversation, win more deals, and create deeper client relationships.

Final Thoughts

The future of lending doesn’t belong solely to cookie-cutter borrowers. It belongs to the self-employed, the creative class, the investor, the newly retired, and the globally mobile. Non-QM loans aren’t just a lifeline—they’re the next chapter in borrower-centric financing.

If you’re not yet incorporating Non-QM into your product strategy, you’re not just missing opportunities—you’re leaving business on the table.

Let AHL TPO help you lead the way. With premium support, scenario review, Non-QM training, and competitive loan programs, we’ll help you originate with confidence.

It’s time to move beyond the myths—and into a market built for flexibility, speed, and opportunity. Let’s originate more—together.

Sources

-

CoreLogic – For performance and default rate data on Non-QM loans post-2015.

-

S&P Global – For market size estimates and Non-QM origination projections.

-

ICE Mortgage Technology – For Non-QM loan share in broker and purchase channels.

-

Nomura Research – For growth projections in the Non-QM securitization market.

-

National Mortgage News – For insights on MBS issuance volumes and investor sentiment in 2023–2025.

-

Fitch Ratings & Moody’s – For credit rating outlooks on Non-QM mortgage-backed securities.

-

AHL TPO internal data – For borrower profile trends, average FICO, loan sizes, and pipeline performance.

-

U.S. Bureau of Labor Statistics (BLS) – For gig economy and self-employment trends.

-

Deephaven, Angel Oak, Invictus, Redwood Trust – For examples of active Non-QM securitization participants.

1